Can you claim before your life insurance starts?

Why talk about interim cover?

Most people do not realise that they might have some protection the moment they apply for life insurance. That is important because underwriting can take weeks or even months, especially if medical checks or financial details are still being processed.

This is where interim cover comes in. It acts as a short-term safety net during that in-between stage before your full insurance officially starts.

“It is one of those things that can really help in that window where clients are waiting for approval. It is not your full policy, but it can make a huge difference if an accident happens while you wait.”

What interim cover is

Interim cover is temporary protection that insurers provide while your application is being assessed. Think of it as a bridge between the day you apply and the day your policy is issued.

Most interim cover is accident-only, meaning it applies if something unexpected happens like a car accident, fall, or major injury. It does not usually cover illness because medical underwriting has not yet been completed.

Azaria explained that there are a few exceptions, but they are still very limited.

“In general, interim cover is almost always accident-only. TAL is slightly different because it will cover trauma events that do not have a three-month qualifying marker. So paraplegia from an accident could be covered, but illnesses like cancer, heart attack, or stroke would not be.”

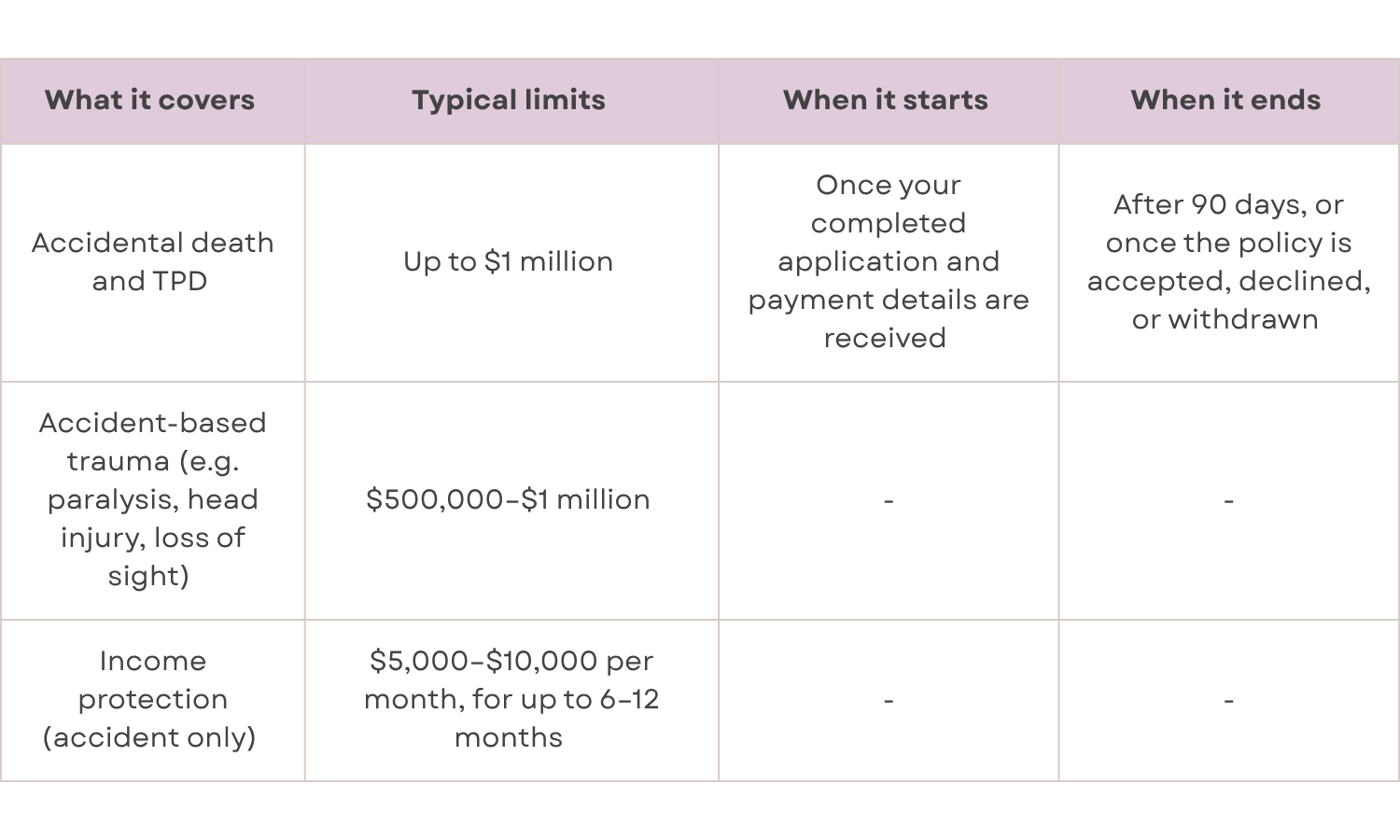

What it typically covers

Here is a simple overview of how interim cover usually works across major insurers in Australia:

Some insurers also offer Interim Rollover Cover, which can extend protection for 30 days once your terms are set but you are waiting for a superannuation rollover.

For families, interim child cover is limited. Only a few insurers include accident-based child trauma, and the cap is often small, around $10,000 to $20,000.

When interim cover starts and ends

Timing varies depending on the insurer.

For most, interim cover begins once a fully completed application and payment details are received. Others, like OnePath, even start it the moment an application is submitted online, before the tele-interview is finished.

It usually ends at the earliest of:

90 days from the date the insurer receives your completed application

When the insurer accepts, declines, or cancels the application

When you withdraw your application

Why insurers offer interim cover

Insurers offer interim cover because they know accidents can happen during the waiting period. It is their way of protecting clients during that small but real window of risk between applying and approval.

“From an insurer’s perspective, they want to make sure people are not unprotected during the process, especially if they are waiting on medical results. It is good for the client, but it is also good business for them.”

How to avoid being exposed too long

The interim cover window is not meant to be stretched out. The goal is to get your full policy active as quickly as possible.

Delays in submitting documents or booking medicals can leave you in that half-covered stage longer than necessary.

Here are some ways to keep the process moving:

Submit your application early.

Provide payment authorities right away.

Book medical interviews as soon as possible.

Follow up with your adviser about outstanding forms or reports.

“Sometimes people think they are fine to wait, but the longer the process drags, the more exposed they are. We want clients to be fully covered, not just under interim terms.”

What it does not cover

Interim cover is limited. It is not designed to replace your full insurance.

The exclusions list is usually detailed and may include:

Illnesses that develop after the application date

Activities not insurable under standard policy terms

Pre-existing conditions

Some replacement policies (depending on the insurer)

According to MoneySmart (2024), interim cover is a “temporary protection mechanism that provides limited benefits while underwriting is in progress.” It should always be treated as a bridge, not the destination.

Real client stories

At Skye Wealth, Azaria and Phil shared stories that show why timing and accuracy matter.

“One of my clients was in the middle of applying for cover when their child developed a rash. A trip to the doctor revealed leukemia. They had to relocate interstate for treatment, which will likely last a year.”

Because the family’s full policy was not yet in force, the child was not eligible for cover at that stage. It is an emotional example of how unpredictable life can be and why completing the process quickly is critical.

Another case involved a client whose application was declined during underwriting because of an unresolved medical investigation.

“He applied for full cover, but underwriting was delayed due to rheumatology tests. Later, he was diagnosed with Psoriatic Arthritis and became uninsurable while his medications were being trialled. We set up accident-only cover, and now, 18 months later, we are looking at full cover again.”

These examples show that timing and follow-up make all the difference.

The takeaway

Interim cover gives you immediate, short-term protection while your application is being processed.

It is valuable, but it is not complete.

If you are applying for insurance, ask your adviser:

What interim cover do I have while I wait?

When does it start?

What events or conditions are excluded?

“Interim cover is a bridge, not the destination. It gives you some peace of mind right away, but the goal is always to get your full insurance active as soon as possible.”

Resources

APRA (2024): Life Insurance Claims and Disputes Statistics

Australian Institute of Health and Welfare (AIHW, 2024): Causes of Injury in Australia