Not all trauma policies are created equal

A real-world comparison of health fund, direct and retail trauma cover

Trauma cover, also known as critical illness insurance, is one of the most claimed types of personal insurance in Australia.

It pays a lump sum if you are diagnosed with a specified medical condition such as cancer, heart attack or stroke. That money can be used however you need. Medical costs, time off work, mortgage repayments or recovery support.

But here is the uncomfortable truth.

Not all trauma policies are created equal. The wording inside your policy can be the difference between a straightforward payout and a painful surprise.

“The trauma definitions are the most important part of the policy. It’s got really nothing to do with the insurer or the premiums you pay. It’s the devil in the detail.”

On the surface, trauma policies can look similar. They all promise to pay if something serious happens. Once you read the definitions closely, the gaps start to appear.

Why wording matters more than brand

Trauma insurance is a benefit-based policy. It pays when you meet a definition. That definition is everything.

“Dealing with clients over many years, especially the last five or six months, I’ve come across a lot of people who have existing trauma policies. They all come from different insurers, being from a health fund, from a direct insurer, or reviewing what we already have in place.”

When definitions differ, outcomes differ. And most policyholders do not discover that until claim time.

“Not all trauma policies are created equal. The wording in your policy can be the difference between a straightforward payout or a painful surprise.”

Heart attack definitions: small words, big consequences

Heart disease remains one of the leading causes of illness in Australia. According to the Australian Institute of Health and Welfare, cardiovascular disease affects hundreds of thousands of Australians each year.

So how does trauma cover respond?

Some policies require multiple diagnostic criteria and ongoing confirmation weeks after the event. Others focus on immediate measurable indicators such as enzyme levels and imaging evidence.

“Six weeks is a long time. The tests they rely on initially are things like troponin levels, which rise and fall in the first 24 to 48 hours. Six weeks later may not actually reflect a minor or silent heart attack.”

If a policy requires retrospective evidence that may no longer be clinically relevant, it creates unnecessary hurdles.

A clearer definition reduces uncertainty. A restrictive definition increases it.

Stroke: what if you recover quickly?

More than 100 Australians experience a stroke every day, according to national health data.

Some trauma policies require permanent neurological impairment lasting a defined period before they will pay.

Others focus on confirmed diagnosis via imaging, without requiring permanent incapacity.

“I read that there was a stroke claim that was declined because the policy required permanent impairment. The more modern definitions talk about confirmed diagnosis based on imaging, without needing permanent incapacity.”

The difference is subtle in wording, but significant in outcome.

If someone receives prompt treatment and makes a strong recovery, a permanent impairment requirement may prevent payment altogether.

Cancer definitions: where most claims occur

Cancer represents the majority of trauma claims across the industry.

That makes cancer wording arguably the most important section of any trauma policy.

Melanoma definitions differ significantly. Some policies pay partial benefits at earlier tumour thickness. Others require more advanced staging.

Prostate and breast cancer definitions can be even more restrictive.

In some cases, early-stage breast cancer only triggers a payout if a total mastectomy is performed.

“That really concerned me. Where they actually wanted surgical intervention in terms of removal or a mastectomy before they paid.”

Modern treatment decisions are based on clinical best practice, not insurance definitions. If policy wording forces surgical thresholds, it may not align with current medical standards.

Neurological conditions: friendlier wording versus exclusions

Conditions such as Multiple Sclerosis and Motor Neurone Disease highlight how different definitions can be across policies.

Some provide clear diagnostic pathways aligned to specialist confirmation.

Others exclude certain neurological conditions entirely.

Most consumers would assume these core conditions are covered automatically. That assumption can be risky.

Procedures and structural heart conditions

Angioplasty and cardiomyopathy definitions also vary.

Some policies pay partial benefits for single-vessel procedures and full benefits for multi-vessel intervention.

Others require three or more arteries before any benefit is payable.

Some exclude the procedure altogether.

When definitions hinge on the number of vessels treated rather than the seriousness of the event, complexity increases.

Price versus wording

A common assumption is that removing advice reduces cost.

A simple pricing scenario was modelled:

• 40-year-old male

• Non-smoker

• Office occupation

• $200,000 Life cover

• $200,000 Trauma cover

• Linked policies

The results were:

• Health fund option: $92.43 per month

• Direct insurer option: $68.52 per month

• Retail advised option: $65.91 per month

The policy with the most restrictive wording was the most expensive.

The most comprehensive definitions were attached to the lowest premium.

“That competition drives price down. The insurer who works with advisers and competes in that marketplace was actually the cheapest.”

Price alone is not a reliable guide to quality.

Older trauma policies: when to keep, when to review

If you already hold trauma cover, replacing it is not automatically the right move.

“If your definitions are better than what’s available today, then we’d suggest you potentially keep it. If your health has changed since you took it out, changing it may result in exclusions or loadings.”

Older policies can contain strong legacy definitions.

However, some newer policies reflect medical advancements and improved clarity.

The only way to know is to compare definitions side by side.

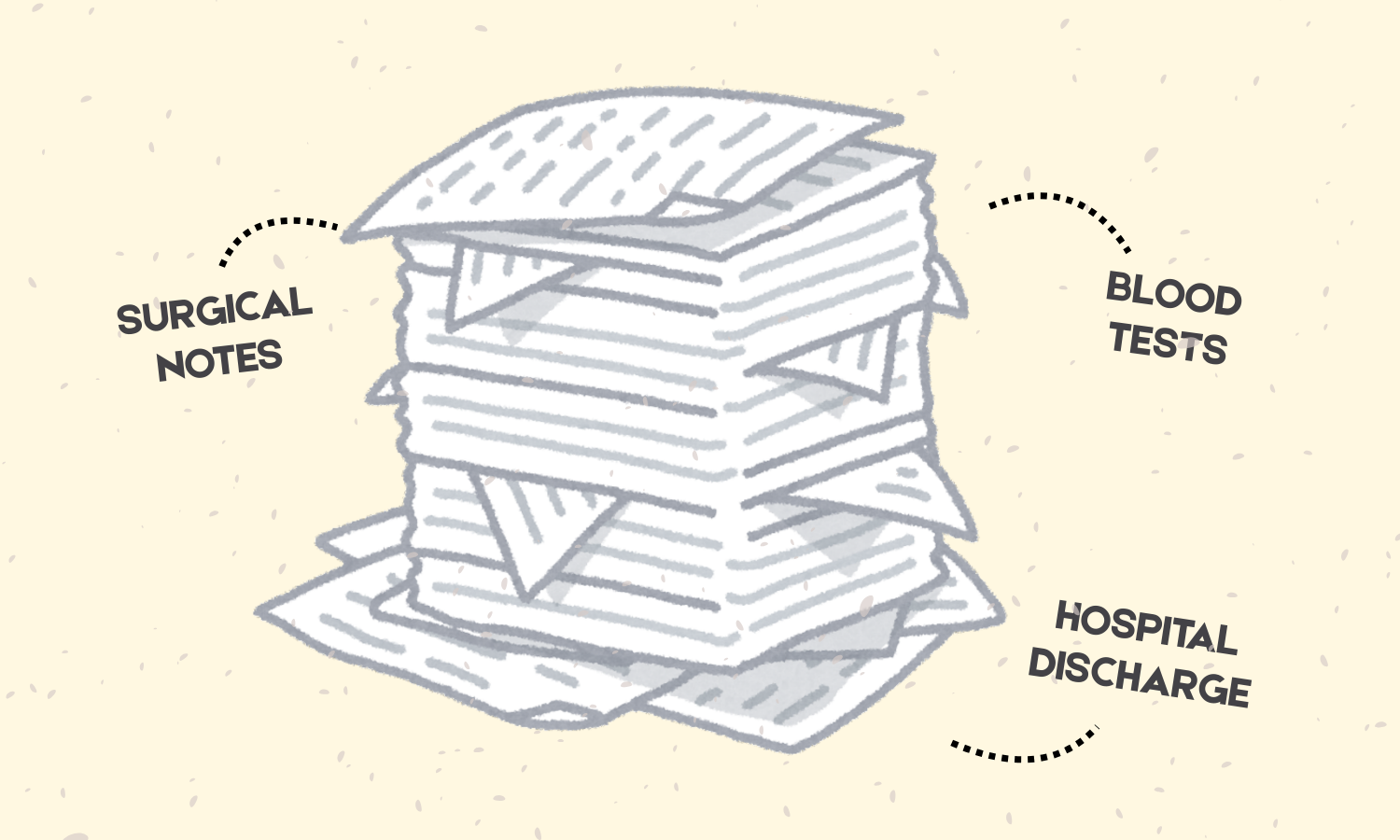

What to gather if you need to claim

Trauma claims are diagnosis-based.

Clear documentation helps streamline the process. This may include:

•Specialist diagnosis letters

• Pathology and blood tests

• Imaging such as MRI or CT scans

• Surgical notes

• Hospital discharge summaries

“If you think there is an event that is claimable, start collecting your documentation as soon as you can. That will streamline the process.”

The regulatory layer most people never see

All Australian life insurers operate under the Life Insurance Code of Practice issued by the Financial Services Council. They are also subject to prudential oversight and claims reporting requirements through the Australian Prudential Regulation Authority.

This means there are baseline standards around fairness, transparency and claims handling.

However, the Code does not standardise trauma definitions.

Policy wording, medical thresholds and evidentiary requirements can still differ significantly between providers. APRA’s Life Insurance Claims and Disputes Statistics also show that claims experience varies across insurers and product lines.

In other words, regulation sets the floor. Definitions determine the outcome.

The key takeaway

Trauma cover is only as strong as its definitions.

It is not about the logo on the policy. It is not about assumptions. It is not even always about price.

It is about whether the wording aligns with real-world medical events.

Because on diagnosis day, wording is everything.

Resources

Financial Services Council. Life Insurance Code of Practice

https://www.fsc.org.au/policy/life-insurance/code-of-practice

Australian Prudential Regulation Authority. Life Insurance Claims and Disputes Statistics

https://www.apra.gov.au/life-insurance-claims-and-disputes-statistics

ASIC MoneySmart. Life Insurance Overview