Can you claim a tax deduction on your financial advice fee?

Short answer? It depends on what kind of advice you’re getting—and how it’s structured.

“I pay my adviser every month—can I claim that?”

If you’ve got an ongoing fee arrangement with your adviser—like monthly or annual payments for regular advice—the ATO says you may be able to deduct it, if it helps you gain or produce assessable income. (SOURCE: TD 2024/7)

✅ That includes advice tied to investments or income protection strategies.

🚫 It doesn’t include general goal-setting, budgeting, or “feel-good” planning.

So if part of your advice is about insurance (like income protection or TPD), it gets a tick. If it’s purely about saving for a Europe trip? Not so much.

“We often split the fee based on how much time or strategy is spent on deductible topics—like income protection inside super.”

What about initial or one-off advice fees?

The ATO says initial advice fees are usually not deductible—because they’re considered capital in nature. (SOURCE: TD 2024/7)

BUT! There’s an exception if part of the advice relates to tax strategies.

For example:

Increasing your TPD cover inside super to deal with potential tax on withdrawal

Setting up income protection with premium deductibility

Making contributions to super to help cover insurance premiums

Adjusting cover to offset tax obligations or benefits

If your adviser is a Qualified Tax Relevant Provider (QTRP), and the advice includes tax-linked strategies, you can potentially apportion that fee.

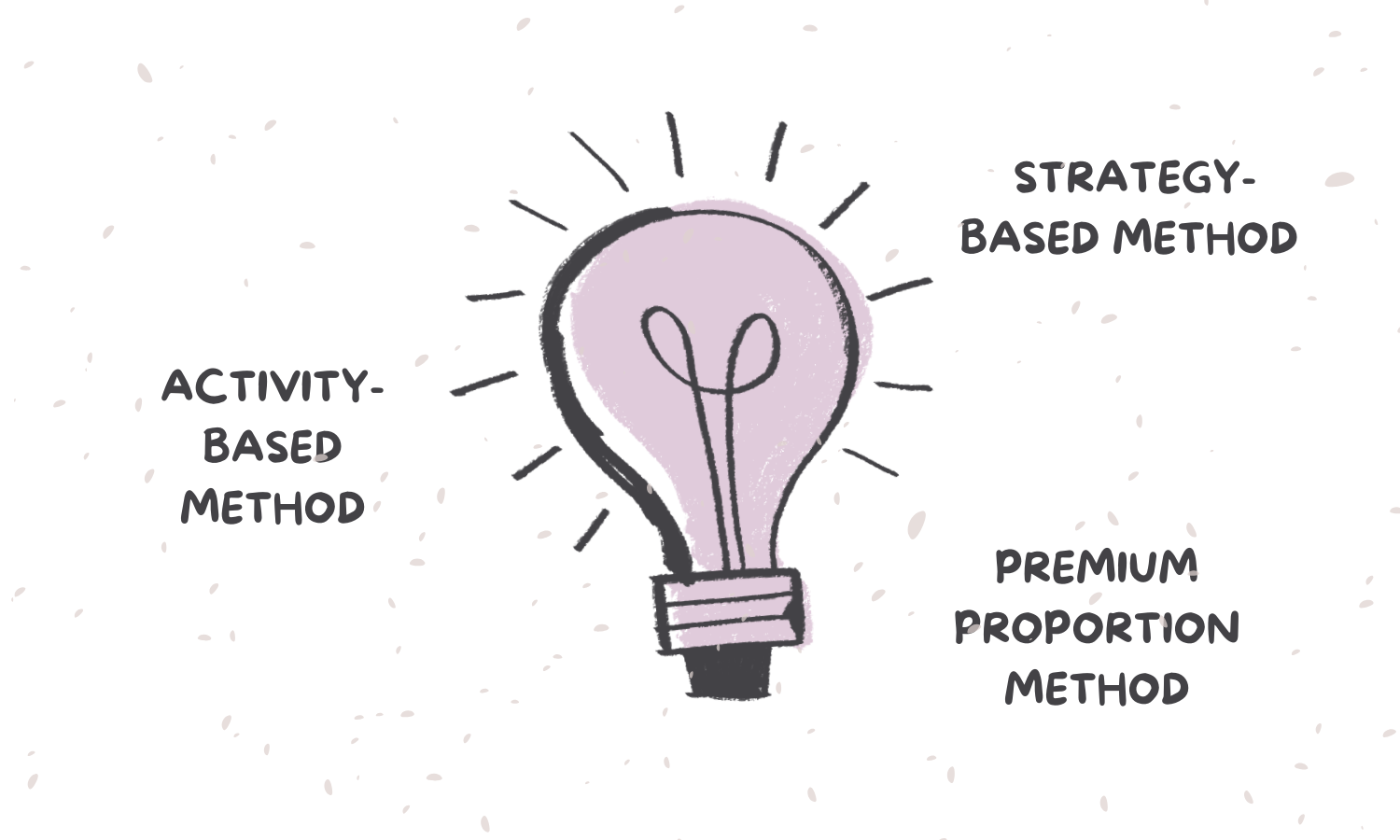

How do you apportion the fee?

There are 3 accepted methods:

1. Activity-Based Method

Split the fee based on how much time was spent on deductible advice.

Example:

Your adviser spends 10 hours on your plan.

2 hours were spent on deductible tax advice.

✅ Result: 20% of the initial fee is tax-deductible.

2. Strategy-Based Method

Work out the cost of advice for each individual strategy. Then, add up the cost of the strategies that relate to tax—that total becomes your deductible portion.

Example:

If the advice for income protection and super contributions makes up a larger share of the work, and those are tax-related, you can deduct the combined cost of those specific strategies—not just divide the fee evenly.

3. Premium Proportion Method

Use the Year 1 insurance premium breakdown to proportion deductible amounts.

Example:

Income protection = $2,000/year

Life & trauma = $4,000/year

You paid $3,000 in advice fees.

✅ Deductible portion: 33% (the share tied to income protection)

Wait—why is income protection special?

Because income protection premiums are tax-deductible under section 8-1 of the ITAA 1997 (SOURCE: Moneysmart).

So, if part of your adviser fee went into setting this up, that chunk is potentially deductible too.

It’s the same with TPD through super, but only the portion linked to tax strategy—like planning for tax on withdrawal.

A quick story from the team…

We often get clients who come to us wanting trauma, life, and TPD—but they don’t realise tax is involved.

“Typically it's gonna be life cover, permanent disablement, trauma, income Protection... and super contributions to cover those insurance premiums.”

At Skye, we spend a lot of time on income protection. It's the most complex part of our advice, and:

“Everything else is just built around our income Protection, so that’s the main part of our advice.”

When it comes to working out what portion of the fee is deductible, here’s how we think about it:

“We are saying that our fees are gonna be 65% tax deductible, and the remaining 35% is non-deductible.”

And the secret?

“Documenting everything and making sure that... at the end of the day, it's up to the accountant to make their assessment.”

We don’t guess. We apportion based on actual strategy—not just the outcome.

“Initial advice fees aren’t a write-off by default. But if you’re getting tax advice—especially around income protection—it pays to ask. ”

What doesn’t count?

General budgeting and financial goal-setting

Home loan broking

Insurance advice with no tax element

Fees for setting up trauma cover only (no tax deductibility)

If there’s no tax strategy involved, there’s no deduction. Simple as that.

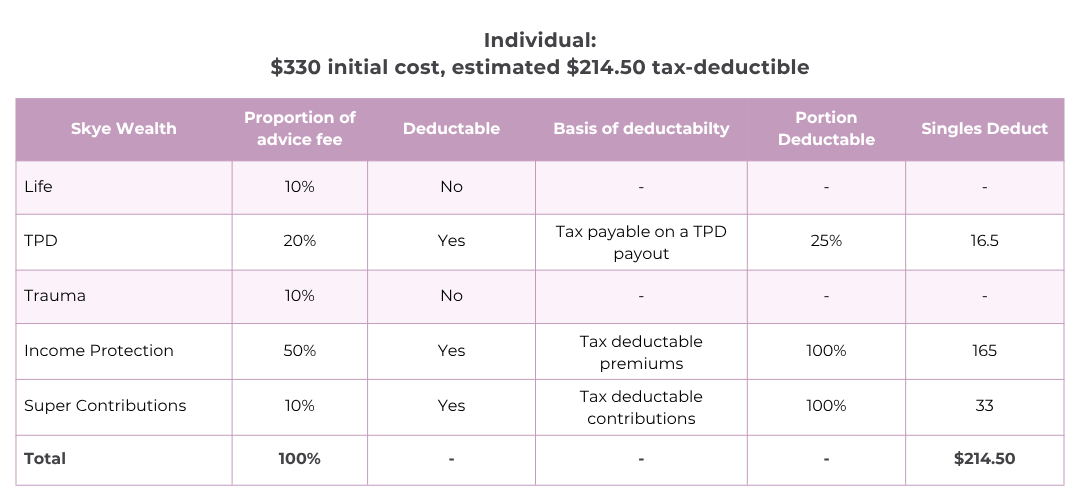

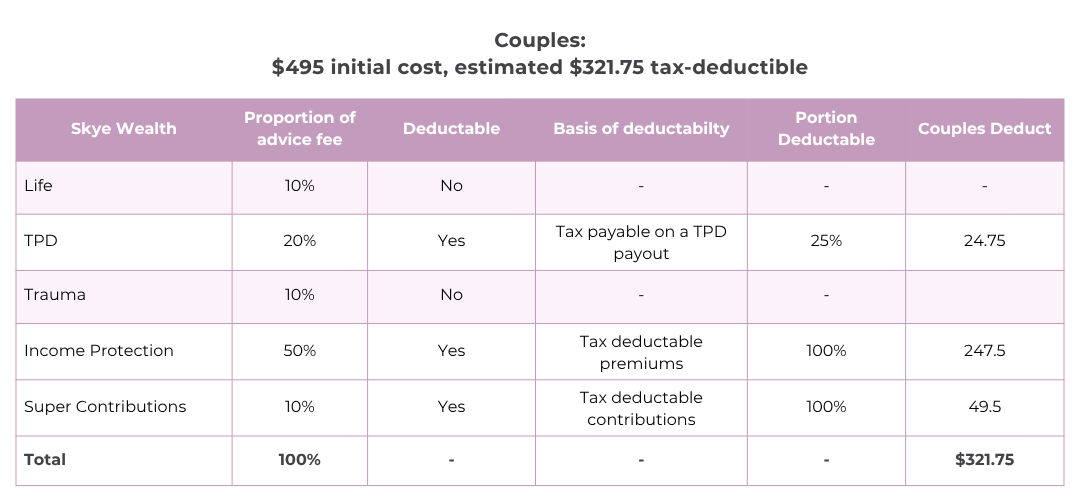

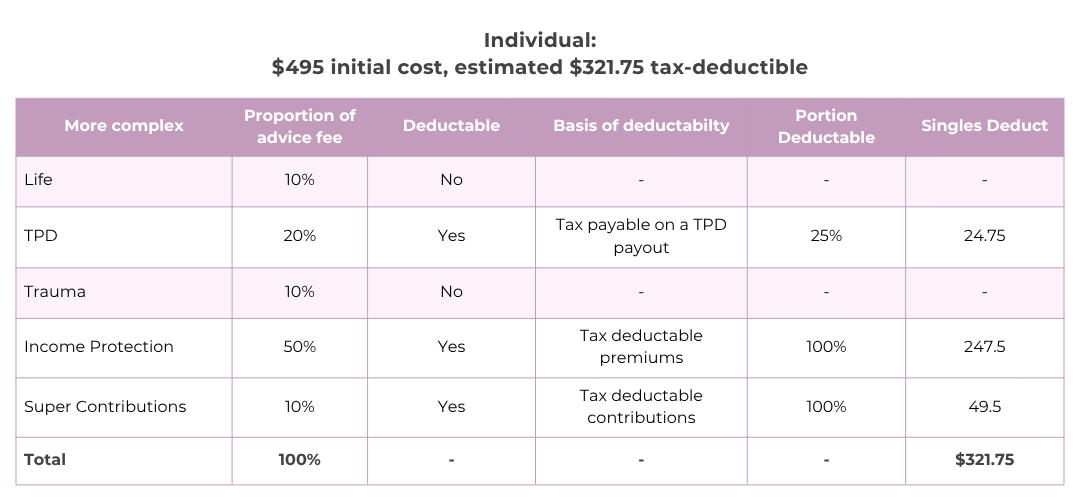

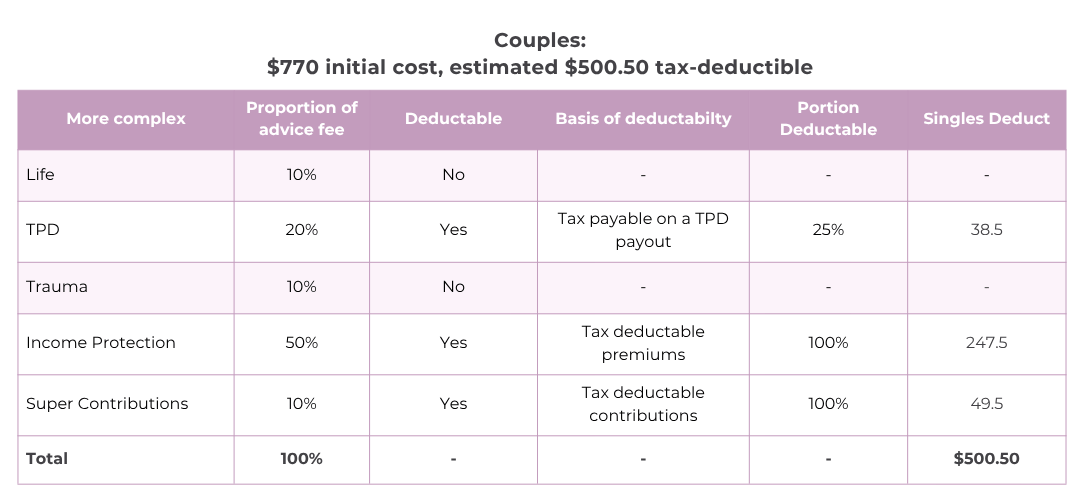

Based on your fee with Skye

If you’ve received insurance-related advice through Skye in the past year, we’ve already done the hard part—breaking down which strategies might be deductible.

Here’s what that might look like:

Single client scenario: up to $214.50 may be deductible

Couple scenario: up to $321.75 may be deductible

More complex advice scenario (higher-value premiums): up to $335–$715 may be deductible depending on cover

These amounts are based on strategy-specific apportioning—not guesswork. We document the work we do for each component, so your accountant can make the final call.

Tax deductibility examples based on Skye advice

Under TD 2024/7, tax deductions depend on the type of advice you received and how much of that advice relates to assessable income or tax strategy.

Standard Advice Fees

Self-Employed Advice Fees

In summary, here’s what you can claim

The rules around advice deductions aren’t just dry tax code—they’re a chance to be smart with your money.

Talk to your adviser, track what’s deductible, and don’t let claimable costs slip under the radar.

Want help working out how much of your advice fee is deductible this year? Let’s chat.

Resources

TD 2024/7 – ATO Determination

Moneysmart – Income Protection Overview

Tax Deductibility of Financial Advice Fees (Skye references, May 2025)