Why your TPD definition matters more than you think

Most people have seen own occupation TPD (Total &Permanent Disability) and any occupation TPD listed in their insurance paperwork, but very few understand how big the gap really is.

These definitions decide how you qualify for a TPD claim and whether you get paid, which can mean a difference of hundreds of thousands of dollars.

“When people hear own occupation TPD, they think it is a minor detail. It is not. It has a major impact on how claims are assessed and what you receive.”

The aim of this guide is to break down how each definition works, how insurers differ, and how your job and work status affect whether a TPD claim is successful.

Own vs Any Occupation

Own Occupation TPD pays when you can no longer work in the specific job you were doing before you became disabled.

Any Occupation TPD only pays when you are unable to work in any job that you are reasonably suited to based on your experience, training, or education.

One is job-specific.

The other is broader and harder to qualify for.

Both definitions appear across Australia’s retail insurance providers, but they do not operate the same way across all insurers.

How insurers decide what your “own occupation” actually is

This is where things get tricky.

The definition of own occupation TPD varies a lot between insurers, especially when people work multiple roles, are part-time, or recently changed jobs.

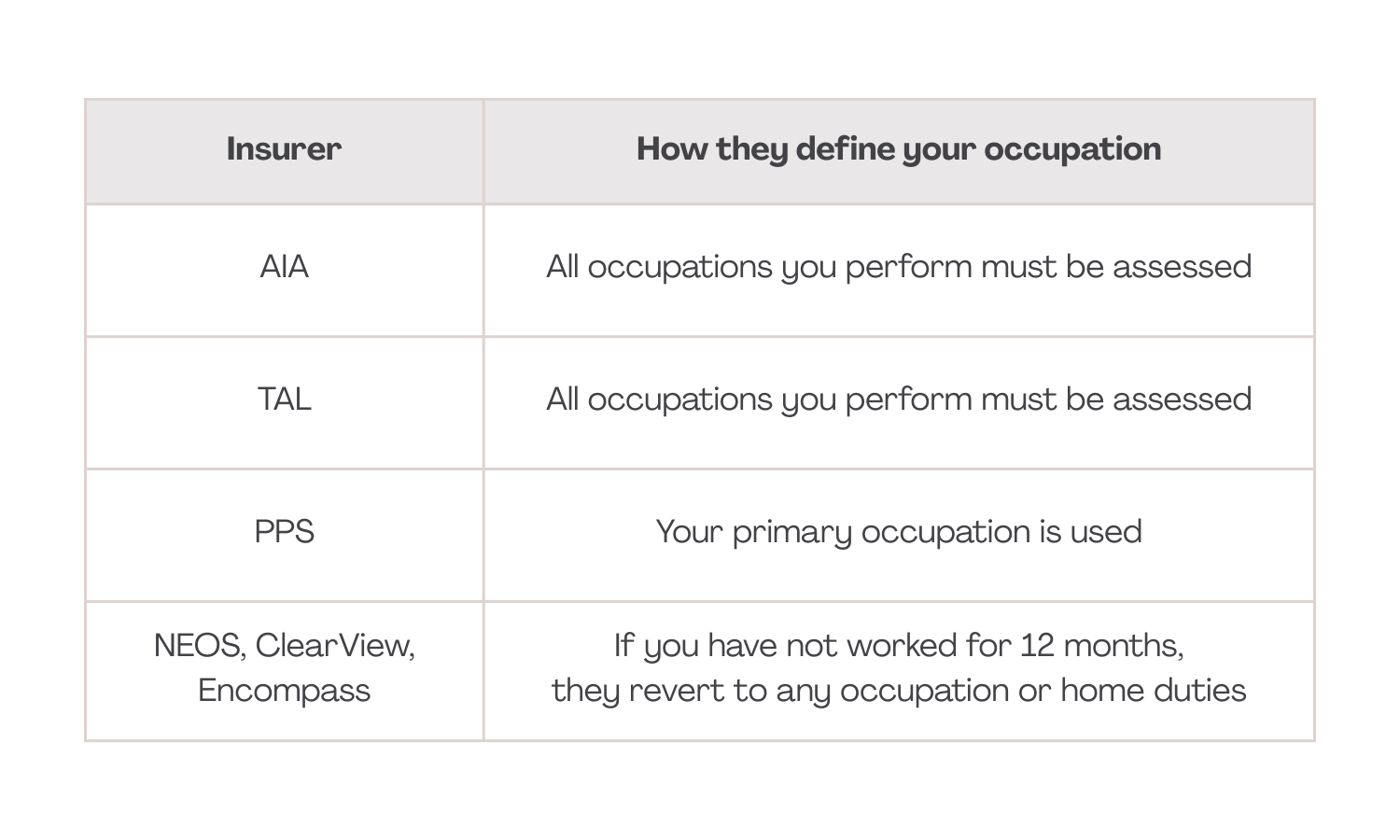

Here is how the major insurers classify occupation for own occupation TPD:

If you work more than one job

Source: Own Occupation TPD Comparison, 2024

This matters because if you have multiple streams of income, some insurers will treat every single one as your occupation at claim time.

For example:

A personal trainer who also works as a receptionist may be assessed under both occupations if insured with TAL or AIA.

But PPS would only assess the occupation where most income came from.

“The job you do most or the job you are paid most for is what counts. Some insurers look at all of your occupations. Others care about just your main role.”

How long do you need to be off work before an own occupation TPD claim is assessed?

This is one of the biggest differences between insurers and the reason own occupation TPD does not always mean what people assume.

Common industry rules

Most insurers require that you are totally disabled for 3 consecutive months before assessing your TPD claim.

This is the same waiting period for both own occupation TPD and any occupation TPD.

One exception stands out:

MetLife

MetLife is the only insurer that says time back at work under a rehabilitation program does not restart the 3-month waiting period.

This can make a major difference for people recovering gradually who attempt a return to work.

Other claim triggers: it is not always about occupation

Some insurers allow you to qualify for TPD even if you could theoretically work, based on other medical criteria.

Examples include:

1. Loss of limbs or sight

Many insurers will pay a TPD claim immediately if you suffer:

total loss of both hands

total loss of both feet

total loss of sight in both eyes

loss of one hand and one foot

loss of one hand and sight in one eye

loss of one foot and sight in one eye

This does not require the 3-month waiting period because it is considered a catastrophic condition.

2. Whole Person Impairment (WPI)

Zurich uses a 60 percent WPI requirement for one TPD definition.

There is no requirement that you stop work, but you must survive for 14 days.

3. 25 percent WPI + Own Occupation restrictions

Some insurers allow a claim if you meet a 25 percent impairment threshold and cannot perform your specific occupation.

TPD is not always cut and dry.

There are several pathways to being assessed as totally and permanently disabled depending on the policy wording.

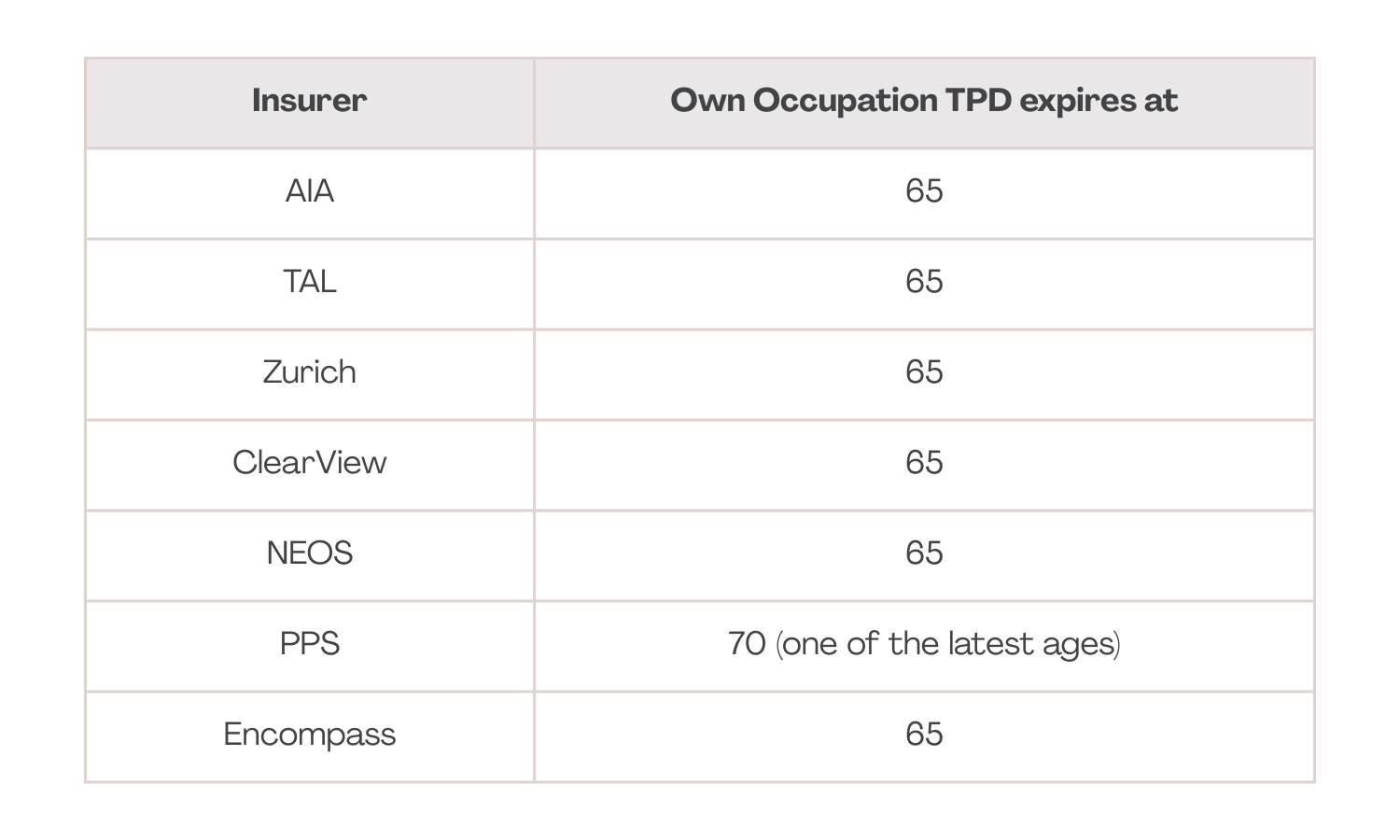

Age matters: when does own occupation TPD expire?

Occupation-based TPD definitions generally do not last forever.

Most insurers stop offering own occupation TPD once you reach certain ages.

Typical expiry ages are:

Source: PDS Extracts, 2024

This means your cover might revert to any occupation TPD past age 65 unless you specifically update the structure.

What about people who were not working?

This is where definitions diverge dramatically.

Some insurers will automatically revert your definition to any occupation TPD if you have not worked in the 12 months leading up to your disability.

This includes:

NEOS

ClearView

Encompass

Others maintain your original occupation definition or focus on your most recent primary job.

This is why stay-at-home parents, carers, or people taking long breaks need extra consideration when setting up TPD cover.

Claim payment benefits: why own occupation TPD is often paid outside super

There is one more major reason own occupation TPD stands out: tax.

If you are assessed under own occupation TPD, the claim bypasses super and is paid directly to you.

This avoids the tax rules that apply when TPD claims are paid through superannuation.

According to the Australian Taxation Office (ATO, 2024), TPD claims paid through super can be taxed depending on your age and service period.

A payment made outside super does not go through that process.

This is one of the biggest practical benefits of having own occupation TPD structured correctly.

Should you choose an insurer based only on TPD definitions?

Short answer: not always.

While TPD definitions are incredibly important, the right choice depends on your job, your income, your risk level, and your long-term needs.

“The goal is not to pick the most generous definition. The goal is to build cover that works for your situation and keeps working long-term.”

Other factors that matter include:

super-linking

tax outcomes

sustainability of premiums

exclusions

whether you hold multiple roles

whether you plan to change jobs

how your claim would be structured

Good advice weighs all of these together rather than just choosing the strongest definition on paper.

Key takeaway

The difference between own occupation TPD and any occupation TPD is more than just wording.

It affects how long you need to be off work, how your job is defined, how claims are assessed, and how payouts are taxed.

Understanding these definitions helps you choose cover that is flexible, protective, and aligned with how you actually work.

Resources

Australian Taxation Office (ATO, 2024). Insurance and tax through superannuation.

APRA (2024). Life Insurance Claims and Disputes Statistics.

Australian Institute of Health and Welfare (AIHW, 2024). Injury and disability data in Australia.